A persistent myth that drivers pay for roads through gas taxes and tolls pervades all discussions on transportation funding, limiting the conversation not just about how we pay for transportation but also what our transportation system looks like.

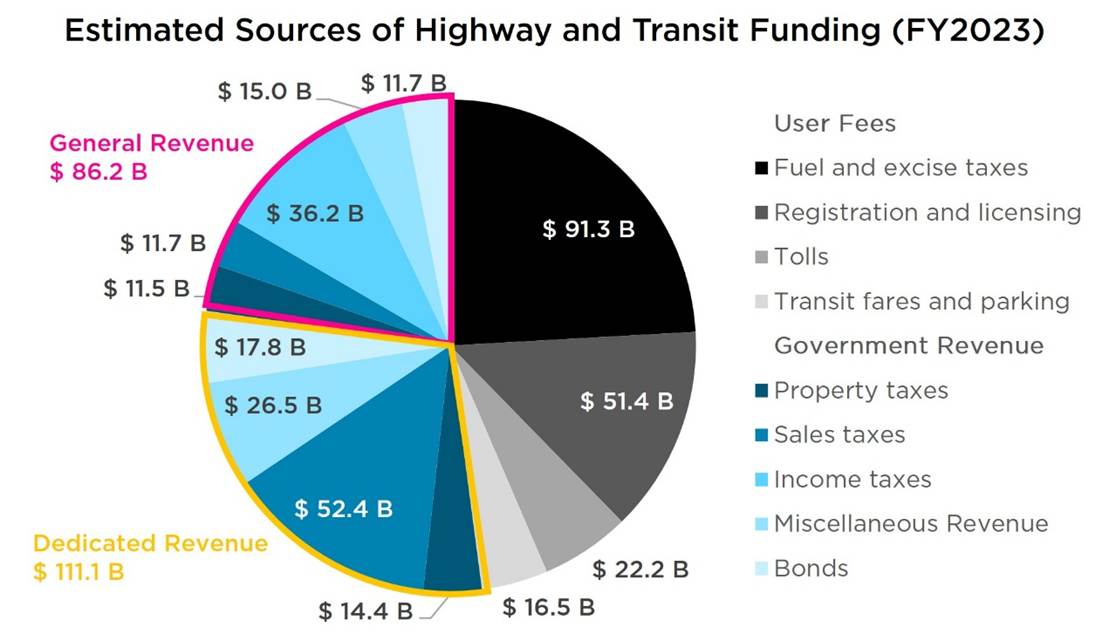

Throughout the history of the United States, our transportation system has been funded through a host of different types of local, state, and federal taxes and fees. Those fees can largely be broken down into three different categories: 1) general government taxes, including property, sales, and income taxes; 2) user fees, which are simply fees assessed on users of the transportation system like tolls and fuel taxes; and 3) Pigouvian taxes, which are a specific category of user fees that respond to an external harm, such as congestion fees and carbon taxes.

The mix and design of these different revenue sources help shape how we think about our transportation system—who pays, why, and how much can set the tone for whose voice is represented in our transportation decisions. It can shape who benefits from our transportation system and who is ultimately responsible for bearing the costs of that system. In this blog, I walk through a number of these funding mechanisms and what each of these choices could mean for creating a more equitable transportation system.

How funding sources contribute to transportation equity

Each of the funding sources discussed below comes with its own choices, including the assessed rate and who its applied to. Those choices have a direct impact on the relative burden placed on any individual or business trying to access transportation services, and that of course means it has an impact on the equitability of our transportation system.

While user fees are not the largest source of revenue for transportation, it tends to be what people think of when they think of transportation funding. While some registration fees may be tied to vehicle value, which could have some tax progressivity, generally user fees are regressive. In the case of fuel taxes, for example, lower-income households spend a larger share of their income on transportation, generally, and on fuel, specifically, which means they are contributing disproportionately to fuel tax revenue. Additionally, because commercial vehicles do not pay their fair share of road use, private drivers at all income levels are effectively subsidizing commercial trucking.

The largest contributor to transportation funding today comes from general funding from local, state, and federal governments, at roughly 23 percent of all transportation revenue, along with an additional 29 percent of revenue that comes directly from a broad range of directed tax revenue, including from property and sales taxes. With each and every one of us having a stake in how we get around, broad public investment in our transportation system is consistent with the role government plays in the shaping of those choices. To the extent that government funding comes from income taxes, the more progressive that revenue source is likely to be. Conversely, the modern shift towards sales taxes as a growing source of government revenue increases the regressivity of government revenues. That means even general government expenditure could be adding to the disproportionate burden faced by lower-income families.

Pigouvian taxes can help shape behavior, and we’re seeing in New York City right now that putting a price on congestion can help reduce emissions and fund much-needed service upgrades for transit. At the same time, these types of taxes can look an awful lot like user fees and often need complementary policies (as in NYC with its low-income discount) to ensure they do not punish individuals facing a transportation system with limited choices.

In approaching efforts to reshape our current transportation system towards one that is more sustainable and equitable and centers people and communities, how we pay for that system must be part of that equity discussion.

Property taxes

The earliest roads in the United States were the responsibility of local governments and required property owners to provide fees and/or labor to maintain the roads. Since the local economy directly benefits from the transportation system through its provision of mobility for jobs outside the local region as well as the support for the influx of customers, goods, and services, it can make sense to tax the landowners benefiting from the value transportation provides. However, today property taxes make up just 15 percent of dedicated local government contributions to transportation and less than 4 percent of all surface transportation revenue and are primarily used for maintenance and operations. Accounting for general transfer from government funds, it is likely around 7 percent of funding, still a far cry from the U.S.’s origins.

👍Taxing land value derives revenue from the individuals and businesses benefiting financially from the provision of goods and services enabled by local transportation infrastructure.

👎A lag in property value increases from improvements can limit transportation development. Property taxes are frequently seen as a regressive funding mechanism for a range of reasons, including inaccurate property assessment, but nuances in local policies have a significant impact on the relative regressivity of specific property tax regimes. Housing restrictions can create regions of haves and have-nots for basic services, as observed during eras of “white flight” to the suburbs or modern NIMBYism.

Tolls

As the United States developed, roads began to play a more critical role in connecting cities, straining local resources for road maintenance and putting more pressure on state governments to facilitate travel. However, in the aftermath of the American Revolution states were still strapped for cash and turned towards private entities to construct and maintain their thoroughfares. From turnpikes (so called because of the pike across the road barring travel until the fee is paid) to the modern toll road, this forces users of the system to pay directly for their travel.

Today, tolls are often assessed differently according to vehicle class, which allows the toll facility to extract some additional funding from commercial vehicles due to the additional wear and tear they impose on the infrastructure. However, tolls generally do not charge for all the costs associated with vehicle traffic such as those related to congestion and pollution. They currently fund just 6 percent of transportation.

👍Charging users directly for road usage creates a direct relationship between the provision of a service and its cost, like many other public services (water, trash, electric power, etc.).

👎Tolls create a pay-for-play system that inherently favors higher income households and can impede mobility access for lower income households. Tolls do not account for the full recovery of all the harms from utilizing our roads and are frequently tied directly to the construction and upkeep of specific infrastructure without consideration of the transportation system holistically.

Registration fees

At the turn of the 20th century, the newly developed motor vehicle numbered in the thousands in the United States. New York was the first state to require each vehicle to be licensed, back in 1901, and with the growing number of vehicles on the road, fees for vehicle registration and, eventually, licensure to drive them, became a growing source of revenue for states funding the proliferation of roads to support these vehicles. Today, vehicle and driver registration fees support about 13 percent of transportation spending.

👍Registration and licensing can serve safety-related purposes.

👎Like tolls, registration and licensing requires financial costs up front to participate in our auto-centric transportation system. While some vehicle registration may be based on vehicle or age and, therefore, may indirectly reduce fees for lower-income households, most states operate on a flat fee basis, making these regressive taxes. Moreover, registration and licensing enforcement can reinforce systemic racial bias through pretextual stops, biased penalties, and predatory fees.

Fuel taxes

Oregon was the first state in the country to implement a fuel tax to fund the development of roadways in 1919, but just a decade later fuel taxes represented over half of fees collected from drivers. The federal fuel tax was introduced in 1932 as part of a revenue act in the wake of the Great Depression but was not dedicated to transportation funding until the creation of the Highway Trust Fund in 1956. Over the course of the 20th century, highway expansion in the United States was funded primarily through fuel taxes, and today fuel taxes account for about 24 percent of spending on roads.

Not all fuel taxes are targeted towards the highway system, however. Some state and local governments dedicate a portion of fuel tax revenue towards general spending, though it is a much smaller amount than the funding from government coffers towards highways. Additionally, a share of state and federal fuel taxes are dedicated to public transit services (about 14 and 18 percent, respectively) and cover just over 20 percent of transit expenditures nationwide.

👍Fuel taxes are correlated with usage of the service provided, like many other public services, and act both as a (small) incentive to improve vehicle efficiency and as a (small) disincentive against driving.

👎Fuel taxes are priced independently of the costs of oil and highway usage. Moreover, while there is a long history of fuel taxes being used as a revenue generator for government services, the link between fuel taxes and road use has been used (via the user-pay myth) to oppose non-highway transportation spending. Additionally, a disproportionate share of transportation expenditures for lower-incomes are spent on fuel compared to higher incomes, so fuel taxes are regressive.

Sales taxes

With federal fuel taxes unchanged for over three decades and vehicle and fuel taxes across all levels of government providing a reduced share of transportation funding, many states and localities have turned to sales taxes to close the funding gap with sales tax revenue dedicated to state and local transportation funds or even specific projects. In 1998, sales tax revenue accounted for 6 percent of all dedicated transportation funding—25 years later, it accounted for 14 percent. Including contributions from general government spending, sales taxes now likely make up at least 17 percent of transportation revenue.

👍Sales taxes are mode-neutral and raise revenue from participants in the local economy, which is inherently linked to the local transportation system.

👎Sales taxes are even more regressive than fuel taxes and are not tied in any way to transportation use or need.

Congestion pricing

Recently, more attention has been paid to the ways in which price signals via taxes and fees can affect the use of our transportation system. One of the prime examples of this is New York City’s successful deployment of its congestion fee program.

Every vehicle on the road contributes to traffic, and every additional car or truck can slow down the system overall, increasing time for other road users. Congestion pricing is designed to incentivize drivers to either shift travel to off-peak times or find alternatives.

There are many ways of designing a fee, but the important point is that it is tied to traffic flow, either through time (e.g., a different charge for peak vs. off-peak hours), current state of traffic (e.g., dynamic pricing of toll-lanes), or by zone (e.g., a fee for entering congested areas of a city).

Because congestion pricing is a specific form of tolling, some of the same concerns around regressivity/pay-to-play exist. However, exceptions related to income, as in the case of NYC’s program, can help mitigate some of these concerns. Additionally, directly connecting the funding from congestion pricing to the support of alternatives can help facilitate a transition towards less harmful, more equitable choices like transit.

👍Congestion pricing helps internalize the implicit subsidies our transportation system provides to drivers, better ensuring drivers pay for the real costs of driving. Additionally, most frequently congestion pricing revenues are used to directly fund alternatives, expanding mobility options for a region to help reduce the harms of high-impact traffic areas.

👎Congestion pricing raises many of the concerns of general tolling, so it can be regressive if additional countermeasures are not taken to mitigate these issues.

Carbon taxes

Another unpriced cost of our auto-centric transportation system is the harm from vehicle emissions. All vehicles on the road produce pollution in the form of tire and brake wear, and all combustion vehicles further contribute tailpipe pollution—all of these forms of pollution result in health harms for the local communities living near our roadways. Additionally, transportation is the largest source of heat-trapping emissions in the United States.

One of the major reasons we have such a fossil-fuel dependent transportation system is because all these harms related to vehicle pollution are not priced into the cost of transportation—drivers may pay for gas, but they don’t pay for the health costs for communities owed to the particulate matter from their tailpipes, and they certainly don’t pay for increased risks of wildfires and other climate-related disasters owed to the hundreds of billions of gallons of gasoline we combust every year in this country.

Pigouvian taxes are fees designed to internalize costs related to a cost currently uncaptured by the market. Carbon taxes are one of the most prominent ideas for how to shift the external costs of climate change back onto the source of climate pollution—in transportation, for example, drivers don’t currently pay for all the climate-related costs of driving, but if we actually added to the price per gallon of gas the monetized climate harms burning that gas in an automobile caused, that would provide a greater signal to the market to use it more efficiently and/or find alternative solutions.

👍Carbon taxes help internalize the implicit subsidies our transportation system provides to drivers, better ensuring drivers pay for the full costs to the climate resulting from driving.

👎Many of the drivers of our fossil fuel dependence are systemic, so carbon taxes run the risk of placing a regressive tax on households without choice. Mitigating this impact may involve economic rebates and/or tying revenue to more sustainable alternatives. Further, carbon taxes only address one of the many forms of pollution from vehicles; additional or expanded policies would be required to ensure the full suite of harms are addressed.

Mileage-based fees / road user charges

Fuel taxes are an indirect fee for road use—more efficient vehicles use less fuel to travel the same distance as less efficient vehicles but may result in comparable wear and tear (within similar vehicle classes). If one is interested in directly allocating the costs of the infrastructure to a vehicle, it may be preferable to simply directly charge users for that upkeep through a mileage-based fee, also referred to as road user charges (RUCs) or a vehicle-miles traveled (VMT) fee.

Some RUCs may be weight-based, which better allocates the wear and tear of the trucking industry on our nation’s roads. While there is no federal RUC, the Department of Transportation has funded a number of state-based pilot programs.

👍Road user charges provide a more direct connection between funding and use than fuel taxes. Additionally, because higher-income households travel more miles and have more efficient vehicles overall, shifting from a fuel tax to a RUC can be a progressive act.

👎Because a greater percentage of purchases for low-income households are in the forms of goods rather than services, RUCs focused on the most damaging vehicles (commercial trucks) can be even more regressive than general sales taxes.

Personal and corporate income taxes

General government funding represents the largest source of funding for transportation today, and for most states as well as the federal government, the largest source of tax revenue for this spending are taxes on personal and corporate income.

👍Income taxes are generally the most progressive tax, with rates typically increasing for higher income thresholds.

👎Exemptions for capital gains or the treatment of business income/losses can significantly reduce the tax rate of wealthier households, flattening the overall tax code.

It’s not just about where the money comes from, but where it goes

There are a host of different ways government and transportation agencies raise revenue for the provision of services, but no matter the revenue source, our system is defined by where that revenue is spent. While most sources of revenue are regressive, progressive distribution of those revenues prioritizing the mobility of lower-income households can help drive towards an equitable transportation system.

While some funding mechanisms may send price signals to users to make more sustainable choices, it’s impossible to take a choice that isn’t available. And so many around the country right now have either the option of an extremely expensive and burdensome car-dependence or underfunded transit alternatives with lengthy headways and/or insufficient coverage to access jobs and other important destinations.

The latest projections from the Congressional Budget Office continue to show that federal revenue does not match federal spending, and at current levels the system is likely to break down by 2028. As I’ve noted throughout this series, funding has failed to keep pace with our choices. But ultimately, what will bankrupt the Highway Trust Fund is not that we have failed to increase fuel taxes—it is that we have failed to support a broader array of mobility choices.

Whether the funding comes from more equitably charging drivers for their impacts or simply by digging even deeper into the Treasury coffers, the next surface transportation bill needs to fund a more holistic, diverse transportation system. Or we will continue to fail to provide folks in the US with the freedom to move.